Jyske Bank will effectively pay borrowers 0.5% a year to take out a loan

Jyske Bank is the first mortgage lender to offer a negative rate. Some banks are considering moving to negative rates on deposits.

Photograph: Alamy

A Danish bank has launched the world’s first negative interest rate mortgage – handing out loans to homeowners where the charge is minus 0.5% a year.

Negative interest rates effectively mean that a bank pays a borrower to take money off their hands, so they pay back less than they have been loaned.

Jyske Bank, Denmark’s third largest, has begun offering borrowers a 10-year deal at -0.5%, while another Danish bank, Nordea, says it will begin offering 20-year fixed-rate deals at 0% and a 30-year mortgage at 0.5%.

Under its negative mortgage, Jyske said borrowers will make a monthly repayment as usual – but the amount still outstanding will be reduced each month by more than the borrower has paid.

“We don’t give you money directly in your hand, but every month your debt is reduced by more than the amount you pay,” said Jyske’s housing economist, Mikkel Høegh.

In recognition of how puzzling the new mortgage is for customers, the bank’s FAQ is littered with questions and statements such as Hvordan kan det lade sig gøre? (How is that possible?) andJa, du læste rigtigt (Yes, you read that right).

The mortgage is possible because Denmark, as well as Sweden and Switzerland, has seen rates in money markets drop to levels that turn banking upside-down.

Høegh said Jyske Bank is able to go into money markets and borrow from institutional investors at a negative rate, and is simply passing this on to its customers.

But the flipside is that savers will see nothing paid in interest on their deposits – and may also suffer as they go negative.

In Denmark, interest rates on savings deposited in Jyske – a Danish equivalent to Halifax or Nationwide in the UK – have already fallen to zero. Now banks in Denmark are thinking of following Switzerland and moving to negative rates on deposits.

“Right now, for deposits we don’t have a negative interest rate. But discussions are ongoing at the very highest level. It’s just that no bank here wants to be the first mover into negative deposit rates,” said Høegh.

While the Bank of England’s base rate is 0.75%, and the European Central Bank’s main rate is zero, in Denmark (which is not in the eurozone) the equivalent rate is -0.4%.

In reality, the Jyske mortgage borrower in Denmark is likely to end up paying back a little more than they borrowed, as there are still fees and charges to pay to compensate the bank for arranging the deal, even when the nominal rate is negative.

Sign up to the daily Business Today email or follow Guardian Business on Twitter at @BusinessDesk

In the UK, although the Bank of England has not cut its base rate, the yields on bonds in money markets have, as in the rest of Europe, fallen heavily, with gilts trading at record lows. While no one is predicting negative interest rates on UK mortgages, banks have begun cutting rates on fixed-rate deals.

Barclays this week cut rates on 15 of its mortgages, leapfrogging its rival NatWest to the top of the best-buy tables on five-year deals.

Three years ago, when gilts yields in the UK were last at the levels common today, NatWest warned its business customers that it may have to charge for accepting deposits, although the charge was never actually introduced.

Welcome to the Smarter Living newsletter! Every Monday, Tim Herrera emails readers with tips and advice for living a better, more fulfilling life. Sign up here to get it in your inbox.

I’m calling it right now: This is the summer of bad personal finance advice.

An industry of experts exists to advise us on how to spend our money. Some of those experts are truly on your side and sincerely want to help you be better with money. Some of those experts are … not exactly on your side, and are perhaps more interested in riling us up about our spending. It can be difficult to tell them apart, and it makes our already-fraught relationship with money even worse.

Earlier this month CNBC generated an outrage cycle about money advice by tweeting this story, in which the personal finance professional Suze Orman claimed that buying coffee means “you are peeing $1 million down the drain as you are drinking that coffee.” (Even the legendary writer Susan Orlean weighed in.) Earlier this summer, USA Today generated a similar negative buzz when it published an article from the money website The Motley Fool that claimed Americans waste an average of $18,000 a year on “nonessential items,” which they said included personal grooming, gym memberships, restaurants, coffee and lunch. These are all on top of similarly shaming articles that tell us we’re not rich because we sleep in and travel; because we buy shoes and jeans; and, of course, because we buy too much coffee.

While it is true that every one of us — including yours truly — can and should be smarter about spending, these small, sometimes necessary purchases are a just a sliver of a much wider story about our struggles with money that, in large part, can be traced back to the Great Recession, the debt load for younger Americans and broader trends about wage stagnation.

“For Americans under the age of 40, the 21st century has resembled one long recession,” the Times columnist David Leonhardt wrote earlier this year. “I realize that may sound like an exaggeration, given that the economy has now been growing for almost a decade. But the truth is that younger Americans have not benefited much.”

To get some answers, I talked to an actual expert who is on our side: Tara Siegel Bernard, a personal finance reporter for The Times and one of the sharpest minds working in this space. Below is a conversation I had with her about the state of personal finance advice, along with what we can do to truly improve our financial well-being. (And let me know on Twitter what money-saving tips have worked for you.)

Tim Herrera: So I feel like we’re in this weird bubble where a lot of personal finance advice is centered around tiny expenses, like coffee, snacks, occasional lunches or other small indulges. I hate it! Those are usually the things that make life worth living! So I’ll start with the question we’re all wondering: Will skipping coffee make me a millionaire?

Tara Siegel Bernard: The short answer: no. It’s silly. It’s a superficial way to get at the “needs versus wants” question, but it’s not a particularly smart one. Or maybe it’s just easier to blame people for overspending on coffee because it’s a lot more difficult to give advice on the many things they cannot control: wages not keeping pace with the cost of living, the high cost of health insurance, housing, child care, paying for college, etc. But … coffee! You can control the coffee!

All of that said, we should try to be thoughtful about spending. We’re constantly making choices and trade-offs that affect our financial and emotional well-being. Should I pay more for housing so I can live closer to work and spend less time on the train and more time with family and friends? Or should I pay less for a home but increase my commuting stress? Those types of financial decisions — how much house to buy, for example, or buying a more economical car — will go a lot further than agonizing over lattes.

[Like what you’re reading? Sign up here for the Smarter Living newsletter to get stories like this (and much more!) delivered straight to your inbox every Monday morning.]

TH: Yes! And I feel that focusing on tiny purchases just ends up making people feel bad and shamed about their spending — like there’s something wrong with them because they lack the willpower not to buy a latte. We all have enough anxiety about money, why does this stuff keep coming up?

TSB: It seems like a quick fix, something we can easily control. But I’m willing to bet that the headlines that accompany these types of stories and tweets generate a lot of clicks.

TH: So while we’re doing a little myth-busting, are there any other especially bad pieces of money advice that have seeped into the public consciousness you’d like to shoot down?

TSB: There’s a myth, or at least a misunderstanding, that investing needs to be hard and complicated, or that you will do better with the more “sophisticated” investments that wealthy people have access to. It’s just not true. If anything, it’s often a marketing tool to push some newfangled mutual fund or investment that you just don’t need.

There is a learning curve, even with the most basic investments, for those just getting acquainted with saving and investing. But it can be boiled down to the following: Buy a collection of low-cost investments like index funds, which will track different certain segments of the stock and bond markets, that provide exposure to businesses around the world. The most important factor is coming up with the right mix of aggressive investments (stocks) and conservative ones (bonds) that you can stomach — and there are smart financial pros who can help you with that.

The quality of any advice you receive depends on who is providing it. Wall Street regulators just passed new rules that, advocates say, may make it even more difficult to distinguish between which financial pros are acting in your best interest. The onus remains on us to sort it all out.

TH: Clearing away all the clutter, very simply: What are a few things average people could do today or this week to improve their overall financial well-being?

TSB: It has become much easier to be an unconscious spender. Within a relatively short period of time, subscription-based businesses are everywhere, and they’re probably betting that most of us will forget to turn off these services when we don’t need them anymore. Unsubscribing to something is a quick little win. It’s not going to make you a millionaire, but you can comfortably buy a cup of coffee with the proceeds. You might also check out our 7-day Money Challenge, which helps you tackle one simple task each day to help improve your financial life.

Here’s another easy one: Do you know what sort of perks your employer provides? Do you commute to work? Do you plan on buying a new pair of glasses? Your employer might have programs that allow you to buy all of these things with money from your paycheck before it has been taxed. If you’re in the 24 percent tax bracket, that translates into a $24 discount on your $100 prescription sunglasses. You might also be able to set aside up to $5,000 pretax for child care expenses. Open enrollment for all of these things — commuter programs, flexible spending, dependent care accounts — tends to happen in the fall, so check with your employer if you haven’t already signed up.

Earning more money always helps, too. Keep a written record of your accomplishments at work and ask for raises when you can build a case. Research shows this can be particularly tricky for women, which is something I’ve written about over the years. (Here’s some advice on asking for a raise.)

It’s also worthwhile to take a deep dive into your finances once every three to five years to get a better grasp on where your money is going and how it’s working for you. I’m a fan of getting advice from a professional, even if it’s only occasionally, to help hold you accountable. (Just be sure the adviser promises to act as a fiduciary, which means your interests are always put first.)

TH: Last question: What’s one piece of financial advice you wish you had known at the start of your career?

TSB: I wish I would have been better at seeing how much more I could’ve saved and invested. I think I knew that I had to save enough to get a matching contribution from my employer, but I should’ve tried harder to see how much further I could’ve gone. It might not have been much, but it would’ve raised my consciousness on the whole “save early and often” idea, and how much that can help later in life. Just going through the exercise helps.

How to Keep Bedbugs From Coming Home With YouBedbugs peak in the summer, just in time for vacation. Here’s how to check your hotel bed for bloodsuckers — and what to do if you find them.

How to Organize Your Messy Contacts List The contacts list on your phone is probably less a list of people you talk to and more a list of everyone you’ve ever talked to. Here’s how to clean it up.

A Misfit’s Guide to Navigating the Office It’s possible to survive — and even thrive — as a misfit without forcing yourself into a round corporate hole. Here’s how to embrace your weird and successfully navigate the workplace.

This week I’ve invited the writer Foram Mehta to give us a little lesson on the art of not butchering someone’s name.

During roll call, my teachers used to pause before sputtering out a chopped-liver version of my name. At appointments, interviews and coffee shops, it suffers a similar treatment. (That’s if people don’t freeze, waiting for me to break the painful silence.)

Butchering someone’s name is the ultimate of bad first impressions. So ensues a domino effect of uncomfortable social exchanges that at best sour someone’s day and at worst deem a relationship dead before it’s had a fair shot. “What’s in a name?” Shakespeare challenged. Well, easy for him to say. Try these tips next time the cat’s got your tongue over an unfamiliar moniker.

Don’t Assume

English class taught us to “sound it out,” but people’s names — especially those roughly transliterated from other languages — play by their own rules. Simply put: If you’re unsure if you know how to pronounce it correctly, you probably don’t.

Just Ask

The simplest solution of all is simply to ask, “How do you say your name?” Doing so is not only respectful, it saves about 10 minutes of correcting, joking and pretending the whole situation isn’t just awkward.

Spell It Out

If afforded the luxury (or if all else fails), there’s always the option of taking it letter by letter. Chances are the person whose name you handled with such tender care will make themselves known midway and, most important, be so grateful.

Like you and every other person in the world, I am no good at New Year puritanism. Two months in, I’m still often drunk and just as unfamiliar with kettlebell squats. That’s also true of this year; but toward the end of 2018, I decided to actually stick to another resolution. Thanks to my more sensible friends living within their means for the first time in our lives, my light financial neurosis recently morphed into full-blown economic anxiety.

So, I decided to start saving and thought I’d take the most extreme route to fiscal responsibility to force me into doing it properly.

Founded in America in the 1990s, the “FIRE” movement stands for “Financial Independence, Retire Early.” You’ll recognize its main principles in that breed of 23-year-old who’s managed to buy a two-bedroom apartment and they never have any fun. Adherents try to save 50 percent or more of their earnings each month, with the aim of hoarding enough cash to be able to invest it, quit their day jobs, and live off interest and dividends. Many don’t fully retire once they reach this point, using their investment to free themselves from office jobs so they can focus on doing stuff they actually enjoy.

My salary is just under the London average of £34,000 [$44,711]. Taking half my monthly wage for saving, along with rent, bills, and monthly subscriptions like Netflix and Spotify, I’m left with £377 [$495] for the month—a budget of around £12 [$16] a day to cover food, travel, and any other expenses.

My first week’s budget is almost blown out by the post-midnight beers I buy in the blurry hours between New Year’s Eve and New Year’s Day. To balance it out, I spend the rest of the week either at work or at home, not spending much, and not really doing much, either. Time stretches out when you have nothing to do. I spend it the same way I did when I was a student—drinking tea and telling myself I’ll start reading a book after I’ve finished the next game of Fifa.

One aspect of the FIRE movement that appealed to me was its anti-consumerism. A number of the blogs I read argue that if only we bought less and stopped caving into immediate desires for things, we could save more and abandon the daily grind. Some combine the FIRE movement with environmentalism, arguing that if you buy less stuff you can save money and the planet at the same time. The lifestyle is often painted as a mixture of stoicism and financial savvy; I envisage myself as a modern-day Henry David Thoreau-type, living deliberately in the wilds of Zone 2, frugally saving half my paycheck and subsisting off of beans and pita bread until I’ve amassed a small fortune that will see me into early retirement.

“If you agree with the fundamental idea that spending doesn’t bring lasting happiness, then in some ways the other stuff comes more easily,” says Barney Whiter, who runs FIRE blog The Escape Artist.

Although he has an anti-consumerist mindset, Whiter says his frugality was born from childhood experience. His parents bought the biggest house they could afford using the biggest mortgage they could afford, but when a recession hit in the early-1980s they had to drastically cut their spending to make ends meet. How quickly their comfortable life became precarious stayed with Whiter, and he has lived frugally throughout his adult life. Now, at 48, he has been financially independent—meaning he never has to work again—for five years.

Chatting over the phone, I tell him my situation: I’m 28 with no mortgage, nowhere near enough savings for a deposit, and student debt larger than the money I make in a year. “When I started out, I felt like you felt,” he reassures me. “It feels like being at the bottom of Mount Everest looking up at the top, but the trick is to not be overwhelmed and think, Every step I take takes me closer.”

I settle into a new routine during my working days: Getting the bus to and from work (£3) [$4]—sometimes running home to save £1.50 [$1.97]—and eating a Tesco meal deal for lunch (£3) [$4]. I know I should be preparing my own lunches to save an extra bit of cash, but the effort required to save an extra dollar a day doesn’t quite cut it for me. I also split a £20 [$26] to £30 [$39] weekly food shop of basic meals with my girlfriend. My weekday routine means I save around half my daily budget for other stuff—not particularly inspiring, but a solid base from which to build my miserly empire.

Illustration by Dan Evans

Thing is, it doesn’t take long for the romantic version of frugality I’d imagined for myself to dissipate. As I spend my lunch break stolidly working my way through a seventh straight chicken sandwich, I’m reminded of an article I saw about Tory MP Dominic Raab eating the same Pret baguette for lunch every working day of his life. Back when I read it, I marveled at the banality and weird dedication of such pitifully small-time behavior. Now, I was its embodiment.

As well as my diet, frugality also starts affecting my relationships. Getting midweek drinks with friends are off—and even though that’s easier at the start of the year because so many people do dry January—it does make me realize how many of my friends I only really see in the confines of a pub. Going from one or two meals out a week to none doesn’t earn me much credit with my girlfriend, who has already noticed spending more to compensate for my scrimping.

At first, it was easy to fill our weekends by doing free stuff, though a few weeks in they also start to drag. There are only so many free art exhibitions you can wander around before it gets boring. We spend one Saturday getting drunk by downloading some pub and bar apps that give you a free pint just for signing up, while the Dusk app also gives you a free drink a day, but we found the bars it was available in were a bit shitty. Saving money was satisfying, but at the same time, viewing life through the narrow lens of cost/benefit analysis sucked the joy out of it. Far from helping my financial anxiety, it was only making it worse.

“I would stop doing things because I tracked every penny that I spent,” says Huw Davies, who runs the Financially Free by 40 blog. “I took it too far and took value from my life.” Davies admits he was too extreme with his frugality at first—he was so focused on saving up enough to quit his boring sales job that he would do anything to make it happen faster. Eventually, he struck a balance between saving and still enjoying life. For him, frugality boils down to spending on consumables versus spending on experiences. “If I can have an amazing weekend away that I’ll look back on fondly, then I’d much prefer to waste money that way,” he tells me.

I saved £1,000 [$1,315] in my first month of trying FIRE, which is a bit over half my monthly salary. I noticed how much pointless shit I buy during a normal month and how much I could save by not buying so much of it: clothes, food, and things for the house were all easy to cut back on. While it felt good to have so much money left over, saving such a high percentage of my income also felt like an unsustainable grind. Whiter says that’s inevitable on my current salary; the more you earn, of course, the less of a squeeze it is to save a bigger proportion of your money.

Some recent articles on FIRE have been ridiculed—fairly, in my opinion, because their subjects earn six figures, or have received large inheritances. The truth is, FIRE is built on the assumption that you will save and invest more as you progress up the career ladder; given the current state of the journalism industry, I doubt I’ll be earning substantially more any time soon.

If saving half of your mediocre salary seems a bit extreme to you, as it did to me, you might be wondering if there is a middle ground between extreme frugality and carefree spending. Both bloggers I spoke to agree that FIRE isn’t a binary choice—saving 50 percent of your salary each month isn’t the only way to achieve a comfortable future—but you don’t need another article on “money hacks” and the benefits of meal prep to know that you should probably be saving a bit more than you already do. “It’s not useless if you don’t have enough money never to work again,” says Whiter. “Every extra dollar you have gives you more freedom and more choices.”

With global warming triggering the collapse of entire ecosystems, and the constant barrage of other anxiety-inducing news, now does not seem a particularly prescient time to hinge your future on the continuing ability of the global economy to offer returns on your savings at its historic average—and even if it does, some people take issue with the maths behind FIRE.

Writing for Bloomberg, Jared Dillian argues that “the biggest issue with the FIRE movement is that it’s the ultimate bull market phenomenon. FIRE seems to work because the stock market has gone straight up.” He says that even if this continues, using the figures that underpin many of the FIRE movement’s assumptions, “it’s not going to be any fun living on a shoestring budget and watching your nest egg decline in value by 30 percent to 50 percent.” Others still have pointed to ever increasing life expectancy as a problem with FIRE; it’s hard to know whether you have saved enough to retire at 40 if you might live for another half a century.

Beyond the issues with the maths behind FIRE, to me it just doesn’t seem worth it to offset the present in such a drastic way, to reduce life to a series of dispassionate financial decisions, for a shot at something that might never come. “If I just drop dead of a heart attack in six months time, that would be a bummer because I’ve deferred my spending for the future,” says Whiter. “What if I never get to experience that?”

It’s a bright September morning in San Carlos, California, and Masayoshi Son, chairman of SoftBank, is throwing me off schedule. I’d come, as he had, to meet with the people he’s tapped to run the Vision Fund, his $100 billion bet on the future of, well, everything. After almost four decades of building SoftBank into a telecom conglomerate, Son, an inveterate dealmaker, launched this unprecedented venture two years ago to back startups that he believes are driving a new wave of digital upheaval. He has staked everything on its success–his company, his reputation, his fortune. We’d both arrived with the same basic question: Where is this massive vehicle heading? But because I wasn’t the one footing the 12-figure allowance, I understood that I’d be the one to wait.

advertisement

advertisement

In the hubbub of Son’s visit, my 9 a.m. meeting gets rescheduled multiple times until it’s set for 4:30 p.m. When I finally arrive at the Vision Fund’s offices, just off California’s Highway 101, I’m struck by how mundane they are. Son is known for big, showy statements. He reportedly paid $117 million for a home in Woodside in 2013, the highest price ever in the U.S. This glass and concrete building, on the other hand, could be found in any part of suburban America.

The room where I wait is spartan. There is an empty desk in one corner, and a conference table with a fake-wood veneer. I try to read the pale gray scribbles on a whiteboard, hoping they might shed light on what happens in this place, but the surface has been too well scrubbed. The interior glass walls of the conference room have been lined with a white, papery substance that turns anyone on the other side into apparitions.

Finally, Rajeev Misra, CEO of the entity overseeing the Vision Fund, rushes into the room, smiling broadly and apologizing profusely. Misra, who has flown in from London for these meetings, looks exhausted but jacked up, as if he’s gotten a shot of adrenaline. Son has this effect on people. It is an exceptionally busy day at the Vision Fund. Not only is the big boss in from Tokyo, but unbeknownst to me, the team is preparing to announce billions of dollars in new investments: a $1 billion round for Oyo, the Indian hospitality startup; $800 million split evenly between Compass and OpenDoor, two real estate disrupters; $100 million for Loggi, a Brazilian delivery startup. It also would lead a $3 billion round in Chinese startup ByteDance, which makes several popular news and entertainment apps, including TikTok. At the same time, Son and his partners are in the midst of launching a second $100 billion fund, with plans already underway to raise an additional $45 billion investment from Crown Prince Mohammed bin Salman of Saudi Arabia—the Vision Fund’s primary backer. Neither Misra nor I knew it then, but this relationship would soon get complicated.

“So what do you want to know?” Misra says, clapping his hands loudly. “You want the road map? I’ll start from 10,000 feet. . . .”

On the surface, the story of the Vision Fund is about money. How could it not be? The numbers are eye-popping. The Vision Fund’s minimum investment in startups is $100 million, and in just over two years since its October 2016 debut, it’s committed more than $70 billion. Son, 61 years old, will also back companies he likes via SoftBank itself or other means: He’s put some $20 billion–and counting–into Uber and WeWork through a combination of financial instruments. (Son’s machinations have always been highly complex and it’s not worth getting lost in the minutiae; regardless of the means, the deals are at his behest.) His big-money bets agitate the venture capitalists who have long inhabited the dry stretch of lowlands between San Francisco and San Jose, a place where any fund over $1 billion was head-turning as recently as three years ago. Turns out, nobody likes competing with a bottomless-pocketed behemoth. “Have you seen the movie Ghostbusters? It’s like the Stay Puft Marshmallow Man tramping around,” one VC tells me before I visit SoftBank. Then he asks me to ask Misra the question everyone in town wants to know: Who is Son investing in next?

[Illustration: Señor Salme; Source for Big Picture: Savillis World Research. *Estimated investment]

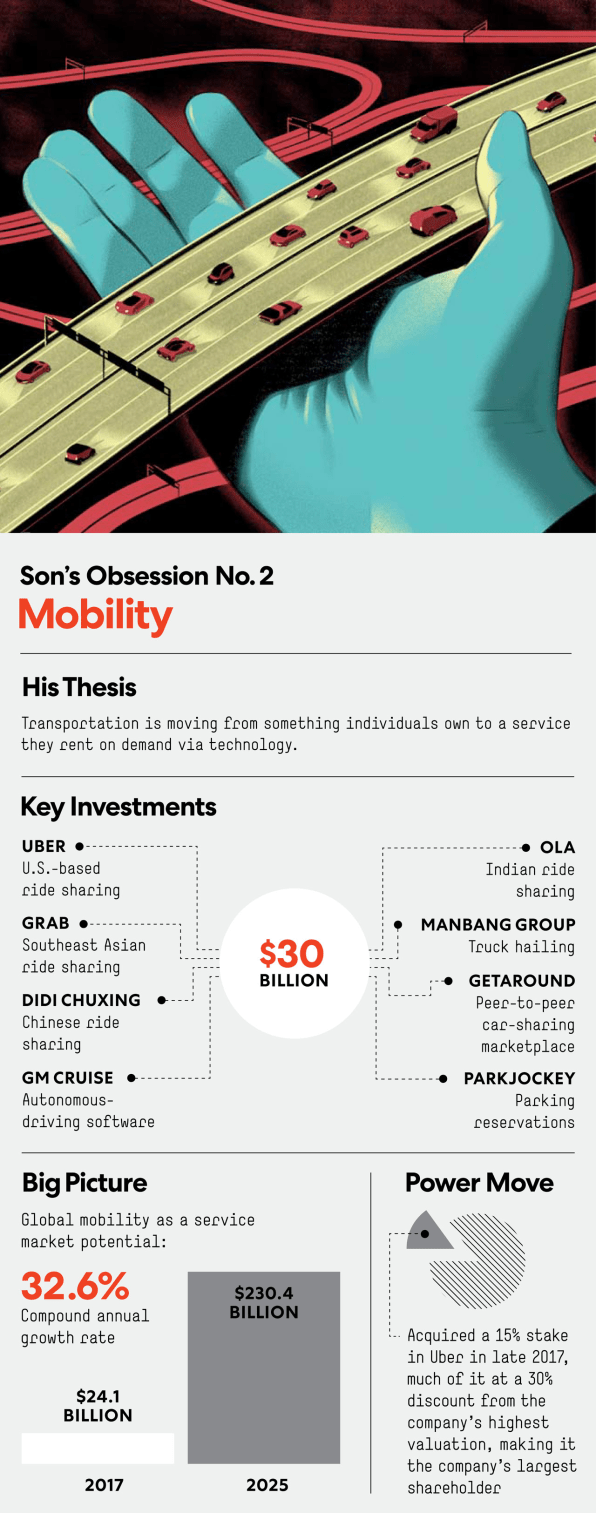

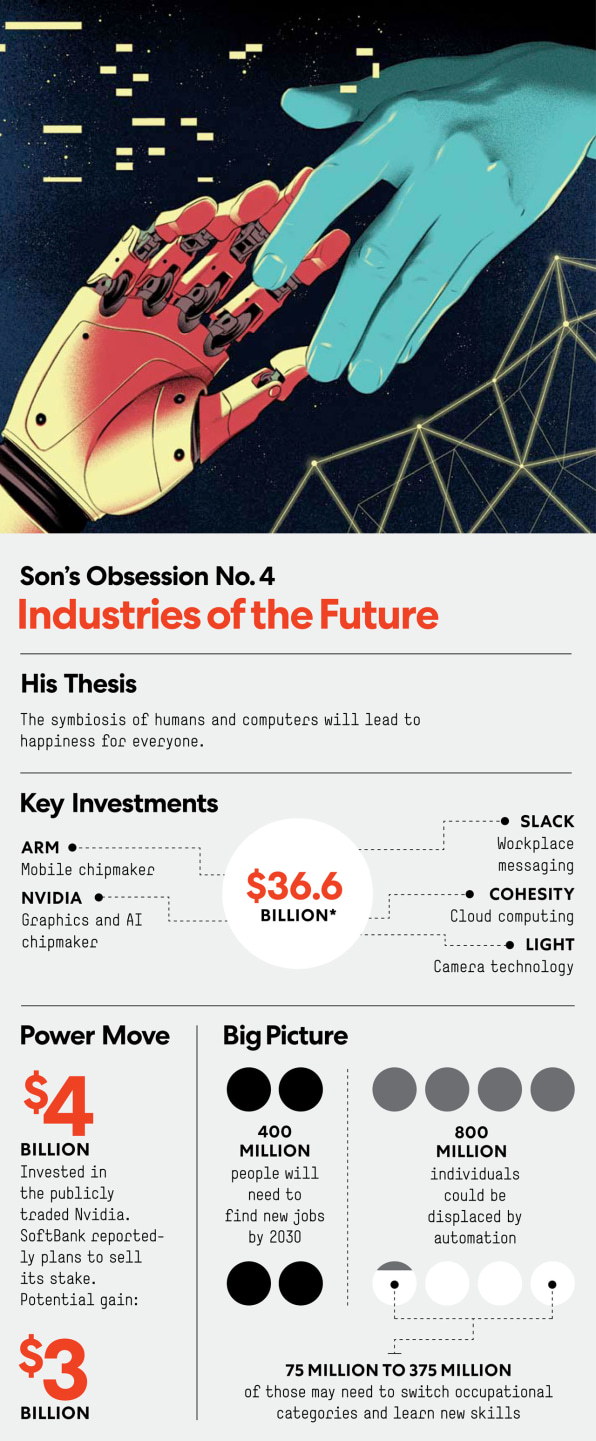

Underneath, though, lies a more complex story. Computers, Son believes, will run the planet more intelligently than humans can. Futurist Ray Kurzweil coined the term “the singularity” to describe the moment when computers take over—and he predicts it will be here by 2040. The Vision Fund could move up this date. And Son is pouring unprecedented amounts of capital into the people and companies employing artificial intelligence and machine learning to optimize every industry that affects our lives—from real estate to food to transportation.

advertisement

When Son first detailed his vision, during an investor presentation in 2010–slides depicted chips implanted in brains, cloned animals, and a human hand giving a robotic one a valentine–there were plenty of scoffs. Many see this machine-driven future as frightening, or even dystopian. But Son believes that robots will make us healthier and happier.

He has long told people, “I have a 300-year plan,” and that declaration is not just the fantastic ambition of a billionaire. He has the means to pursue these dreams, and they’re starting to become very real. He is one of the few people with the power to make decisions that could have global consequences for the future of technology and society for decades, if not centuries. As Facebook and Google have demonstrated, machines take on the attributes of their makers. Algorithms, software, and networks all have biases, and Son likes to bet on founders who remind him of himself, or at least share his ideals. Son’s values, then, will become our own, dictating the direction of this machine-powered world.

So where is this massive vehicle heading?

Our story begins with a dinner Son hosted one summer night in 2016 at his nine-acre estate in Woodside. The table was set in the garden so the guests could enjoy the crisp summer air of a northern California evening, as well as the breathtaking hilltop views of San Francisco horse country.

Among the attendees was Simon Segars, who had no idea when he sat down to eat that this would be one of the most important events of his life. Segars, CEO of chip designer Arm, had imagined that he might win some new business from Son–perhaps SoftBank would agree to put Arm’s chips in the cell phones it sells through its telecommunications businesses. He didn’t fully appreciate at that moment that one of his dining companions, Ron Fisher, has been one of Son’s trusted consiglieri for more than 30 years and is almost always present when Son is considering a major deal. “We started talking about AI and all these future-looking technologies,” Segars recalls, and Son grew visibly animated. They discussed how Arm’s technology could be used to turn anything–tables, chairs, refrigerators, cars, doors, keys–into a wired object. Son pressed Segars: If money were no constraint, how many devices could his technology create? As the leader of a publicly traded company, Segars had never been asked to think this way before. “I remember Simon’s eyes getting very wide,” Fisher recalls.

A few days later, Segars was at his desk when a call came from Tokyo: It was Son, who said he needed to see him and Arm chairman Stuart Chambers right away. Chambers was on vacation, on a yacht off the Turkish coast, but Son didn’t want to wait. He sent a private jet to fetch Segars and persuaded Chambers to dock his boat in the Eastern Mediterranean.

advertisement

[Illustration: Señor Salme; Source for Big Picture: Orbis Research]

The day unfolded like a scene from a James Bond movie: Segars landed at a small airstrip near the village of Marmaris, Turkey, where two security men picked him up and whisked him to an empty restaurant overlooking the marina. (Son had arranged to have it cleared of other customers.) “It was surreal,” Segars says.

Son got right to it: He wanted Arm and was willing to pay for it. In a deal that would astound Wall Street for its speed and audacity, SoftBank offered $32 billion for the company, 43% more than its market value at the time. Son negotiated and closed the deal in two weeks. A photo of that trip to Turkey shows Son standing by the port of Marmaris, boats bobbing on the sea behind him. He is smiling, as though he knows how big this moment is.

To pursue his sweeping vision of interconnecting everyday objects to create intelligent machines, Son would need more money. So he created the Vision Fund. The first investor was the Saudi Arabian Public Investment Fund, with a $45 billion commitment that October. It’s hard to overemphasize the significance of the Saudis coming in at this stage. The entire global venture capital industry invested just over $70 billion annually, so the idea of a single $100 billion fund seemed fantastical. The move conveyed such confidence in Son’s vision and ability to execute on it that it quickly attracted other investors, such as Apple, Foxconn, and Qualcomm. By the following May, the fund had secured $93 billion. As Son explained at the time, he needed this much capital because “the next stage of the Information Revolution is underway, and building the businesses that will make this possible will require unprecedented large-scale, long-term investment.” Now he was ready to start what Bloomberg has called “an all-out blitz on the heart of Silicon Valley.”

When I step off the elevator at WeWork’s headquarters in New York City one Thursday morning in October 2018, a dozen or so children have taken over the reception area. They’re students from WeGrow, an elementary school the company launched a year earlier, and they’re hosting their weekly pop-up vegetable stand. “Would you like to buy something?” asks a girl of around 6 or 7, holding an iPad listing products and prices. I’m here to learn how Vision Fund’s money is being spent and would rather not walk into my meetings holding a head of lettuce, so, feeling like the Grinch, I tell her I’ll pick something up on the way out. She shrugs; there are plenty of other customers.

Sunlight pours in through tall windows overlooking West 18th Street. The open floor plan lets me see from the reception area across rows of tables populated by WeWork members tapping away on laptops. At the far end of the space, there’s a wall of glass, behind which Adam Neumann, WeWork’s CEO, is taking a meeting. He looks like a rock star, with long, dark curls brushing his shoulders, black jeans, and a wide-brimmed black fedora, and as far as the Vision Fund is concerned, he is. “There is a sense of massive opportunity,” says Fisher, who sits on WeWork’s board. Son has even called WeWork his next Alibaba. In 2000, he put $20 million in the untested Chinese commerce startup. Today, Alibaba’s market cap is nearly $400 billion.

WeWork’s potential lies in what might happen when you apply AI to the environment where most of us spend the majority of our waking hours. I head down one floor to meet Mark Tanner, a WeWork product manager, who shows me a proprietary software system that the company has built to manage the 335 locations it now operates around the world. He starts by pulling up an aerial view of the WeWork floor I had just visited. My movements, from the moment I stepped off the elevator, have been monitored and captured by a sophisticated system of sensors that live under tables, above couches, and so forth. It’s part of a pilot that WeWork is testing to explore how people move through their workday. The machines pick up all kinds of details, which WeWork then uses to adjust everything from design to hiring. For example, sensors installed near this office’s main-floor self-serve coffee station helped WeWork discern that the morning lines were too long, so they added a barista. The larger conference rooms rarely got filled to capacity–often just two or three people would use rooms designed for 20–so the company is refashioning some spaces for smaller groups. (WeWork executives assure me that “the sensors do not capture personal identifiable information.”)

advertisement

“We can go to Berlin,” Tanner says, tapping another monitor. He’s now using Field Lens, project-management software that WeWork acquired in 2017. Field Lens helps WeWork track building construction and maintenance. A live image appears. Zooming in, Tanner shows me how the system can pick up granular details about a site. We’re 4,000 miles away, but I see a nail sticking up from a floorboard. “We’ll have to get someone to fix that,” he says nonchalantly.

I ask what else we can spy on. He taps the screen and calls up a large map displaying each of the 83 cities in which WeWork operates. From here, we can drop down into any of them: Around the world in 80 nanoseconds.

“Basically, every object will have the potential to be a computer,” adds David Fano, WeWork’s chief growth officer, who is overseeing development of this new technology. “We are looking at, what does that world look like when the office is this highly connected, intelligent thing?”

[Illustration: Señor Salme; Source for Big Picture: eMarketer and Stratista. *Estimated investment. **Projected]

This is why Son is investing billions in WeWork. As of mid-December, the tally was up to $8.65 billion (including debt and funding of subsidiaries), and the real estate company was valued at $45 billion. [In early January 2019, SoftBank invested another $2 billion.] To meet Son’s lofty expectations, WeWork is spending as fast as it can to spread its footprint. It has more than doubled its locations in the 15 months since SoftBank’s initial investment, and WeWork has acquired six companies and invested in another half dozen. It has grabbed so much office space that it is now the largest commercial tenant in New York City, Washington, D.C., and London. It has expanded into Brazil and India. In the fourth quarter of 2018, the company planned to add more than 100,000 desks. This pace may only accelerate: SoftBank is in talks to take an even larger stake in WeWork for up to $20 billion, according to a source familiar with both companies.

These moves have accelerated WeWork’s revenues but also its losses. In the first nine months of 2018, WeWork shed $1.22 billion, even as it grossed $1.25 billion. The company owes $18 billion in rent from office space it has leased. When WeWork issued bonds last spring to raise another $700 million, ratings agencies labeled them of lower quality, aka junk. “We cannot get comfortable with the company’s financial and operating position, which includes a massive asset/liability mismatch that is usually a recipe for disaster, significant cash burn, cyclically untested real estate business model, and uncertain path to profitability,” CreditSights analyst Jesse Rosenthal wrote at the time. The price of those bonds dropped almost 5% below their list value in their first five days of trading, a signal of investor skepticism.

As a result of WeWork’s hypergrowth, both physical and technological, the company is increasingly viewing itself less as a real estate company than “a spatial platform,” helping connect humans with intelligent machines. A 2018 internal WeWork presentation depicted the scope of the company’s aspirations as a series of concentric circles. On the outermost ring sit its actual business units, from its school to its gym to its live events (such as its annual adult summer camp, a mashup of the Governors Ball Music Festival, Bhakti Fest, and Burning Man). The next layer is the fundamental elements of human existence–live, love, play, learn, and gather–which those products seek to fulfill. Then, at the very center: We.

advertisement

Neumann has always been the kind of entrepreneur who thought about having 100 buildings when he had three, but with Son backing him, WeWork’s expansion has been extraordinary. “Adam and Masa have a special relationship,” says Artie Minson, WeWork’s CFO. Those who work closely with them say Son sees in Neumann a younger version of himself–hungry and willing to move at top speed. Those inside WeWork say that Son’s mentorship has been critical. “He’s helped us move from asset-based thinking, how a building is performing, to how an account is performing,” says Fano, who joined WeWork in 2015 when the company acquired his building management startup. WeWork’s aim, he explains, is to “shed ourselves of any remnants of being like a real estate company.”

“Masa wants to meet with you. Can you get on a plane tomorrow?”

For many, the call to Tokyo comes out of the blue, as it did with Stefan Heck, founder and CEO of Nauto, a startup that builds AI-powered cameras to enable self-driving vehicles. Heck had been preparing for a board meeting and was reluctant to cancel it, but one of his board members told him to get going, saying, “People spend their whole lives trying to get a meeting with Masa.”

Every entrepreneur who receives money from the Vision Fund eventually sits down with the SoftBank boss. The Vision Fund’s 11 partners (based in California, London, and Tokyo) decide which entrepreneurs are ready at a weekly meeting, after months spent getting to know a company and its founders. Usually, CEOs are ushered into a large conference room atop SoftBank’s sleek Shiodome tower in Tokyo, which has expansive views of the harbor and beyond, a metaphor for how Son searches wider than almost all other venture capitalists for his investments. One of Son’s Vision Fund VCs, Jeffrey Housenbold, ex-CEO of the photo service Shutterfly, is leading an effort to build a system to track emerging startups, which he hopes will help the fund identify its next investments even faster and more efficiently.

Son is small in stature and soft-spoken. Those who know him well say he’s quick-witted and humble, with a self-deprecating sense of humor. When friends teased him about his vague resemblance to Charlie Brown, he put a Snoopy doll on his desk. One time, at an investor conference, he called himself “big mouth.” He loves the movie Star Wars. “Yoda says, ‘Listen to the Force,’ ” he told an interviewer, who asked him in May 2018 how he makes his investment picks. He rarely wears suits. When Nauto CEO Heck met Son for the first time, Son was dressed in jeans and slippers. “I have seen young founders come in very apprehensive to meet Masa,” says Fisher, who is often with Son during these pitch meetings. “By the end they are talking to him about their dreams.”

Colleagues say Son is at his happiest when chatting with startup founders–brainstorming, strategizing, inventing. “If Masa could spend the whole day doing what he loves, it would be meeting with entrepreneurs,” says Marcelo Claure, SoftBank’s chief operating officer and the former CEO of Sprint (the wireless carrier that boasts SoftBank as its majority owner).

advertisement

Son is not focused on profit margins during these meetings. What he wants to know is, How fast can the company go? This has a hypnotic effect on his portfolio CEOs. “Masa told me, ‘The entrepreneur’s ambition is the only cap to the company’s potential,’ ” recalls Robert Reffkin, cofounder and CEO of the real estate brokerage platform Compass (who says Son also asked him the question about what he would do if money were no object). Sam Zaid, CEO of the car-sharing platform Getaround, remembers Son inquiring, “How can we help you get 100 times bigger?” before ultimately giving him $300 million in August 2018. Even proven winners are not impervious to Son’s motivational gifts. “It is people like Masa who can accelerate our world,” says Uber CEO Dara Khosrowshahi, who counts Son as his biggest investor. Khosrowshahi says Son’s backing will be key to helping him build Uber into “the Amazon of transportation.” And when Housenbold first met Son, the SoftBank chairman told his future Vision Fund partner, “We are going to change the world.”

Dave Grannan, cofounder and CEO of Light, another startup building 3-D cameras to be the eyes of self-driving vehicles, met the SoftBank leader in Tokyo last spring. (Son’s strategy is to make multiple bets in the same categories; the house wins either way.) Grannan was in Son’s office presenting how his technology works when Son grabbed a camera that the founder had brought with him as part of the demonstration. Son aimed its lens at a picture hanging on the wall, a portrait of a man who looked like a Japanese samurai from long ago. He then handed the camera back to Grannan without explanation. Later, Grannan, feeling that it might be significant, looked up the image. The subject was Sakamoto Ryoma, a famous ronin adventurer who rose from humble beginnings to overthrow the feudal shoguns of the Tokogawa era and launch Japan into the modern age. He is Son’s childhood hero. “Every morning when I come to work, it reminds me to make a decision worthy of Ryoma,” Son once told an audience. “Ryoma was the starting point in my life.”

Son grew up poor on the remote island of Kyushu, in southern Japan. His family had emigrated from Korea in the 1960s at a time when racism and anti-foreign sentiment were rampant. His parents had named him Masayoshi, the Japanese word for “justice,” because they hoped an honorable-sounding name would deflect cultural prejudices that cast Koreans as crooks, liars, and thieves. It didn’t work: Son was bullied at school.

Son drew strength from his relationship with his father, who was convinced that his child was destined for greatness. Once, while in elementary school, Son told his father, Mitsunori, that he wanted to be a teacher. Mitsunori, now 82, told him he was thinking too small about his future: “I believe you are a genius,” he said, according to Japanese biographer Atsuo Inoue in his 2004 book, Aiming High. “You just don’t know your destiny yet.” When Mitsunori was struggling to start a coffee shop, he asked his son to help him find customers. Son told him to offer free coffee to lure them in–and make up the losses once they came through the door. Mitsunori handed out drink vouchers on the street, and soon the café was full.

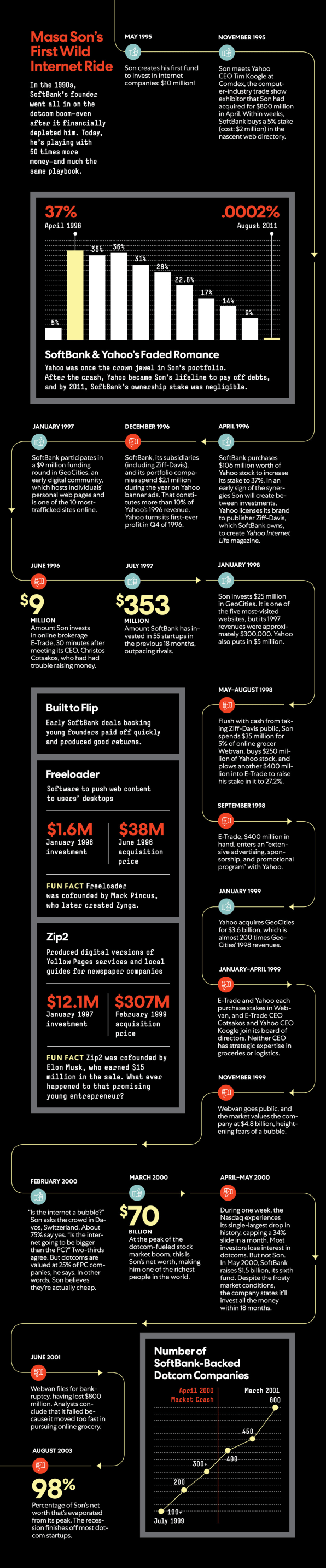

After earning a degree from UC Berkeley in economics and computer science, Son returned to Japan and launched SoftBank in 1981. He had only two part-time employees and no customers, but he had mapped out a 50-year plan for the company that started with selling computer software. It didn’t matter that, back then, very few people had computers and there was virtually no software business. When he told his two employees, “In five years, I’m going to have $75 million in sales,” the pair promptly quit.

advertisement

To drum up business, he even followed the same advice he once gave his father: He handed out free modems on the street. Another time, Son reserved the largest booth at an electronics trade show and spent everything he had on fliers, displays, and a sign that read now the revolution has come. His booth drew a crowd, but still no sales. But he persevered, and by the mid-1990s, SoftBank was the largest software distributor in Japan and Son took the company public on the Japanese stock market.

Son was drawn to the burgeoning internet boom of that era, and his attention turned to the United States. Success with investments in Yahoo and E-Trade led the company to make others, and by 1997, Silicon Valley’s local newspaper labeled SoftBank the most active internet investor. “Our über-strategy is to get everyone’s eyeballs, then their money, then a piece of everything they do,” one of the company’s VCs later told Forbes. In January 2000, two months before the peak of the dotcom era, Son claimed to own more than 7% of the publicly listed value of the world’s internet companies, via more than 100 investments. As Son has told the story, at one point his personal net worth was rising by $10 billion per week; for three days, he was richer than Bill Gates. But SoftBank’s stock slid as investors started to question Son’s relentless dealmaking, particularly his decisions to acquire a bank and bring the Nasdaq stock market to Japan via a joint venture. Rivals and skeptics believed these moves would be used, respectively, to fund SoftBank investments and take them public. Then the U.S. markets crashed, in April 2000, and the stocks of such SoftBank high-fliers as Buy.com, Webvan, and even Yahoo collapsed. Son, a true believer, only sped up his investing in the face of the dotcom apocalypse. By March 2001, The Wall Street Journal reported that SoftBank had bet on 600 internet companies. By that count, he’d more than tripled his exposure in 14 months. During that same time, SoftBank’s stock fell 90%, and $70 billion of Son’s net worth disappeared.

“Most human beings who’ve had the kinds of experiences he’s had become tentative,” says Michael Ronen, who has worked with Son for 20 years, first as a banker at Goldman Sachs and now as a partner in the Vision Fund. But Son, friends say, thrives on the edge. “You’ve never seen someone so fearless,” says Ronen.

Even as Son’s empire was tanking, he invested $20 million for a 34% stake in a then obscure Chinese e-commerce site run by a former teacher. Fourteen years later, when that company, Alibaba, went public, that stake was worth $50 billion.

“Twenty years ago, the internet started, and now AI is about to start on a full scale,” Son told investors and analysts this past November while reporting SoftBank’s second-quarter results. Standing on stage in Tokyo, he laid out the numbers to back up his assertion. Behind him, a slide featured dozens of companies in the Vision Fund’s portfolio, many now valued at more than $1 billion (in part due to SoftBank’s largesse). The Vision Fund’s returns–after selling its stake in Indian e-commerce company Flipkart to Walmart in May 2018–had boosted SoftBank’s operating profits by 62%.

Son and his colleagues refer to his strategy by using the Japanese phrase gun-senryaku, which can mean a flock of birds flying in formation. (Son also refers to his investments as his cluster of number ones.) Collectively, these enterprises are moving faster–and more forcefully–than they ever could individually. Those on the inside say it is even more rapid than anyone on the outside realizes. Over the summer, Son asked Claure, his COO, to start a new internal division devoted to “value creation.” Its purpose is to help Vision Fund entrepreneurs access SoftBank’s vast global resources and partnerships. Claure currently has 100 people working on the team, technically known as the SoftBank Operating Group, and expects to have 250 dedicated to these efforts by sometime next year.

advertisement

A key element of this value creation comes from connecting companies to help each other grow. Son hosts dinners and events to bring people together, and he suggests they use each other’s services (a strategy he also deployed in the 1990s). For example, Compass and Uber rent space from WeWork. Mapbox, an AI-powered navigation system, inked a deal with Uber last fall. Nauto has met with executives from GM Cruise, the self-driving software maker in which SoftBank invested $2.25 billion last spring. Son’s introductions help entrepreneurs feel more connected to a bigger purpose. “The family concept really does work,” says Nauto CEO Stefan Heck. “There is a level of trust among us that we are all building toward this vision.”

[Illustration: Señor Salme; Source for Big Picture: McKinsey Global Institute. *Estimated investment]

One evening last fall, Son hosted a dinner at his home for his senior investing team. Gathered around Son’s dining table, the group discussed the company’s future. Son mentioned some companies he’d recently met with in Asia that were finding new ways to apply artificial intelligence to their businesses. He explained why he believed AI could cross into so many different industries, which spurred a lively conversation about the new opportunities others at the table were seeing. There was a sense of enormous forward momentum. Where else could they go?

Sometimes, though, the universe presents an unexpected detour. Right around the time of the dinner, news broke that operatives working directly for SoftBank’s biggest investor, the Saudi Arabian government, had murdered Saudi journalist (and American resident) Jamal Khashoggi. Almost immediately, Son was thrown into a geopolitical maelstrom. SoftBank’s stock plummeted as investors fretted about the implications of his close ties to Crown Prince Mohammed bin Salman, whom the CIA concluded had personally issued the kill order. Only a month earlier, after committing $45 billion to back a second fund, bin Salman told Bloomberg that without Saudi backing, “there will be no Vision Fund.”

As gruesome details about the murder emerged, the pressure on Son became intense. “Right now, any CEO taking money from SoftBank would put him or herself at risk of an employee revolt,” one top Silicon Valley investor told me a week after the murder. “No one wants to be connected with blood money.” Some of Son’s Vision Fund companies publicly tried to distance themselves from Saudi Arabia (Compass’s Reffkin issued a statement saying, “The death of Jamal Khashoggi is beyond disturbing because the freedom and safety of the press is something that is incredibly important to me.”) Uber’s Khosrowshahi and Arm’s Segars pulled out of a major Saudi investment conference in Riyadh in October. Son did as well, but another Vision Fund partner did participate—and Son met privately with bin Salman that week in Riyadh. What they discussed has not been disclosed, but it is clear that somehow Son was reassured. In November, he announced plans for a $1.2 billion solar grid outside of the Saudi capital. “As horrible as this event was, we cannot turn our backs on the Saudi people as we work to help them in their continued efforts to reform and modernize their society,” Son said in a statement. “MBS seems to be riding out the controversy,” says Karen E. Young, a resident scholar at the American Enterprise Institute, pointing out that for anyone interested in doing business in the Middle East, Saudi Arabia cannot be ignored. “[Son] is a businessman. He is not going to turn his back on $45 billion.”

The global network that Son has built during his four-decade career is as vast–and important to him–as his war chest, friends say. It includes business leaders such as Bill Gates, Warren Buffett, and Jack Ma, and world leaders such as China’s Xi Jinping, India’s Nahendra Modi, and Donald Trump. “You have to remember who helped you along the way and the loyalty that one has to show for your partners during good times and bad times,” says one person close to Son.

Son is working to ensure that the Vision Fund can survive, with or without Saudi money: SoftBank secured some $13 billion in loans from banks last fall, including Goldman Sachs, Mizuho Financial, Sumitomo Mitsui Financial, and Deutsche Bank. Son has also made clear that the Vision Fund is very much open for business, announcing a slew of new deals, including $1.1 billion for View (a maker of “smart” windows), $375 million for Zume (which builds robots that can cook), and that lead investment in ByteDance and its AI-powered news and video apps. “This is just the beginning,” Rajeev Misra tells me in December. Over the next year, the Vision Fund plans to back dozens of new AI-driven startups, almost doubling its portfolio from 70 to 125 companies.

advertisement

There is no one on the planet right now in a better position to influence this next wave of technology as Son. Not Jeff Bezos, not Mark Zuckerberg, not Elon Musk. They might have the money but not Son’s combination of ambition, imagination, and nerve. The network of companies within the Vision Fund, if they succeed, will reshape critical pieces of the economy: the $228 trillion real estate market, the $5.9 trillion global transportation market, the $25 trillion retail business. We won’t be able to turn Vision Fund–backed services and technologies off like computers and smartphones. They will, ultimately, have minds and thoughts of their own.

Of course, Son is not an unstoppable force. Any number of factors–economic downturns, geopolitical crises, government regulators–could upend his best-laid plans. There’s always the possibility he could be betting on the wrong companies. Son, however, doesn’t have time to traffic in doubt. “There are good times and bad times,” he proclaimed when he launched the Vision Fund, “but SoftBank is always there.”