Whether you have a goal to reach $1 million or $10 million, you have to start somewhere.

Thomas C. Corley, a certified public accountant and certified financial planner, spent five years studying millionaires and gathered his insights in multiple books, including “Change Your Habits, Change Your Life.”

Corley interviewed 233 people with at least $160,000 in annual gross income and $3.2 million in net assets, 177 of whom were self-made. Through these interviews and analysis, Corley uncovered dozens of commonalities about rich people and their daily habits to piece together exactly how they got to where they were.

In his book, Corley wrote that 80% of the self-made millionaires he studied didn’t get wealthy until after age 50 — but that almost all of them started the same way.

“The self-made millionaires in my study all set a goal of saving 10 to 20 percent of their income during their pre-millionaire years,” Corley wrote. The average American has a savings rate of about 8%, according to the St. Louis Federal Reserve.

More important, the pre-millionaires were intentional about where they put their savings. Using a strategy Corley calls “the bucket system,” they siphoned their savings into four general categories: retirement savings, specific expenses, unexpected expenses, and cyclical expenses.

Retirement savings includes IRAs, annuities, 401(k)s, and other workplace retirement plans — that is, money invested for growth and to be spent later in life. Future education costs, wedding costs, a home down payment, and other big expected costs are part of the second bucket.

The third bucket is more or less an emergency fund, a separate account with cash to fall back on in the event of sudden job loss or a medical emergency. And the cyclical-expenses bucket contains savings for birthday gifts, holidays, and vacations.

This savings strategy proved crucial for almost half of the millionaires in his study, who he says followed the Saver-Investor Path. They eventually were able to live on 80% or less of their take-home pay, remained consistent and patient, and never flaunted their wealth. Above all, they used time to their advantage.

“Self-made millionaires make a habit of saving,” Corley wrote. “The more you are able to save at an early age, the more wealth you’ll accumulate.”

I hear this question often, and if you’re a parent, you’ve probably Googled it several times yourself.

In my 30 years of professional experience, I’ve worked as an auditor, investor, tax preparer and financial consultant — and I’ve witnessed the impact of financial literacy (or lack thereof) on countless adults of all ages.

Teaching your children about money doesn’t have to be complicated. You either put in the effort and time, or you don’t. And if you do, it’s best to start sooner rather than later. (According to a 2013 Cambridge University study, children are already able to grasp basic money concepts at age three, and by age seven, their money habits are already set.)

How we teach our kids about money

My wife and I have two kids, both under 14. Like most parents, we don’t want them to suffer from financial anxiety when they’re older. Nor do we want them to be in debt and have to eat into our retirement savings.

The same way we want them to understand the importance of telling the truth or saying “please” and “thank you,” we also want them to understand the importance of money: What it’s worth, why it’s important and how to practice smart habits that lead to success.

In order to do that, we keep things fun and simple:

1. We play “Let’s Go Shopping”

I’ve found that my kids are more engaged in the learning process when it’s experimental or gamified. “Let’s Go Shopping” was a game we played when they were in preschool.

After my wife and I priced the items, we had one child do the shopping while the other handled checkout. We stood by to facilitate and answer questions. But eventually, they became skilled enough to play on their own.

Stimulating the shopping experience sharpened their math and budgeting skills. It also helped them feel more comfortable talking to one another about money.

2. We play “How Much Does It Cost?”

A game that we continue to play is “How Much Does It Cost?” (It’s basically our family’s version of “The Price Is Right.”)

At the dinner table, we all take turns presenting arbitrarily selected items for sale, along with multiple choice answers for their approximate prices.

A few examples:

Water bottle: $0.50, $2.50 or $6?

Movie ticket: $4, $10 or $40?

Monthly phone bill: $12, $100 or $400?

New (basic) car: $5,000, $35,000 or $500,000?

Games like this help them understand the relative values of various products and services.

3. We don’t freely give them money

One of the biggest mistakes I see parents making is offering unlimited funds to their children for non-essentials.

Our kids started getting a weekly allowance when they turned six. We’d give them $6 per week and increased the amount by $1 each year they got older. They could earn more if they did something good that week, like offer to help someone or ace a math test.

Of course, there are no set rules as to how much you should give your children; it mostly depends on your financial means and what you expect them to be financially responsible for.

The consequences of giving your children unlimited funds for discretionary spending (especially after they’ve used up their entire allowance) aren’t realized by most parents until much later.

Children of parents who do this may develop the habit of relying on additional funding sources that can be quite costly, such as debt in the form of high-interest credit cards.

4. We guide them through the budgeting process

The easiest way to teach your kids about budgeting is to budget together.

When my kids get invited to a birthday party, for example, I give them a reasonable budget and help them shop for a gift that stays within their price lane. (My wife and I prefer to do this on Amazon because it’s an easy way to teach them how to comparison shop.)

5. We show them how to put their money to work

When my oldest daughter saved up enough money, we relocated her cash from a piggy bank to a local bank.

“Congratulations! You’re putting your money to work,” I said.

Even though the process makes complete sense to you, it might be too abstract for some children. That’s why it’s important to explain — in layman’s terms — how their money is earning more money (passive income) and how that additional money will continue to generate even more money (compounding).

These are concepts and skills that will serve them for life.

6. We encourage them to do good with their money

My wife and I make it a point to donate to charity or a nonprofit organization every once in a while. It sets a good example for our kids and discourages behaviors of selfishness and greed.

When our kids have saved up enough money, we review a list of charitable organizations together (Charity Watch is a good place to start) and have them pick one that supports a mission they value.

This is a great way to teach them about sharing, kindness and how money — whether it’s $1 or $10 — can be used to help others.

One of the most interesting things I’ve found over the years of writing about personal finance, charting my own financial progress and changes, and talking with countless readers is that personal finance is a lot like an onion. An onion? Yep, it’s all about layers.

It’s like an onion in that it’s made up of a bunch of layers that aren’t really very transparent. You know what’s underneath them on some level, but it takes time to really understand each level and incorporate it into your life.

Advertisement

Here, I’m going to summarize some of the layers of the onion so that you can get a good idea of what I’m talking about.

The First Layer: Debt Is Bad, Savings Is Good

This is the level on which many people who are really struggling with their money see their finances. They understand that debt is bad and that saving money is good, but when it comes to the things they want in their life, this seems secondary. Isn’t it much better to just spend that money on stuff that you want? A big house? A lot of stuff to fill it? A shiny car in the driveway?

The basic ideas of personal finance—spend less than you earn, avoid debt with high interest rates, try to save some of the money you make—are actually pretty obvious. Everyone understands those ideas on some level, but they don’t put them into practice.

Why? They don’t really see the connection between their day-to-day behavior and the mountain of debt and the lack of savings that they have.

Advertisement

Sure, they understand the idea, but it’s not incorporated in their life in any way. It’s like a fact that they know, not one that really matters when it comes to their behavior.

Let’s peel back a little bit more.

Advertisement

The Second Layer: Your Choices Create Both Debt and Savings

The next layer of realization is when people begin to realize that the things that they spend money on create both debt and savings. The more money you spend on stuff, the less savings you’ll have and, if you spend too much, the more debt you’ll have. The less money you spend on stuff, the more savings you’ll have and the less debt you’ll have.

Advertisement

In other words, thelittle choicesyou make every day are the determining factor in whether you have debts or savings—and how much of each you have.

Whenever you buy anything, you reduce your potential savings. If you’re in debt, you effectively increase your debt, too, because that money isn’t going into savings or toward your debt.

Advertisement

This goes from the big purchases, like cars and so on, down to the tiniest purchases, like a bottle of soda at the gas station. Each one of those purchases—each one of those choices—has an impact. Whenever you choose to spend—and whenever you choose to spend less or not to spend at all—you shape whether or not you have debt and whether you have savings.

Let’s peel back a little bit more.

The Third Layer: Much of the Stuff You Buy Doesn’t Create Lasting Joy

The counterargument against cutting back on non-essential purchases is that doing so removes the pleasure from life. I’m adamantly opposed to doing that. If a purchase brings genuine, lasting pleasure in your life, you shouldn’t cut it.

Advertisement

The catch is that the vast majority of purchases people make do not bring lasting joy. They bring a little short-term burst of pleasure, but lasting joy? It’s actually pretty rare for that to be the outcome of spending your money.

I went out for dinner last night. The dinner was good—it was pleasurable—but the pleasure of it is already fading away. It was expensive and it didn’t create lasting joy and it won’t be long before I’ll either forget it entirely or regret the expense. On the other hand, my most memorable meal of the last year was one where I ate with an old friend. It did create lasting joy—a meal that we still talk about that reconnected me to an old friend.

Advertisement

If you’re going to spend money on something that isn’t essential, why not spend it on something that has a very high chance of creating lasting joy in your life?

For me, one powerful way to do that was to eliminate my debts and have some money in the bank, because the stress that it eliminated and the small sense of security that it created did in fact bring me lasting joy, joy that lasts to this day.

Advertisement

Beyond that, there are a handful of things in my house that I’ve bought that have brought me lasting joy. Most of them? Maybe I thought they would and they didn’t, but in truth most of them were purchased without even thinking about the question, and now I regret it. That money went away from something that would bring me lasting joy (financial independence) into something that doesn’t (many of the items in my home).

Let’s peel back a little bit more.

Advertisement

The Fourth Layer: Money Can Buy Time

Most of the things that bring lasting joy in my life require the contribution of time to bring that joy. My relationship with my wife is joyful because I invested time into that relationship. My relationship with my children is joyful because I’ve invested time in those relationships. Some of my key hobby purchases have brought me lasting joy because I’ve invested time in that hobby.

Advertisement

A random meal at a restaurant rarely brings lasting joy because you didn’t commit any time to it. On the other hand, a meal eaten with a friend—no matter where it is—can often bring lasting joy because you’ve built that relationship. It doesn’t matter where you eat, because the value comes from the thing you invested time in—that friendship.

Many people feel very time-deprived and they often use their money to buy time, but the question becomes how they use that time that they save. A person might buy some convenience foods to save on meal prep time, but how do they use that time?

Advertisement

There are some things you can always do with that extra time to provide lasting value. You can rest. You can build a lasting relationship with someone. You can learn a new skill or some key knowledge.

The thing is, money can certainly buy time, but it similarly becomes a waste if you don’t do anything valuable with that time.

Advertisement

Let’s peel back a little bit more.

Advertisement

The Fifth Layer: Money Can Buy Freedom

Spending money to buy time in the form of time-savers like convenience foods and time-savings services is a great way to get some spare time in the short term, but it doesn’t help with the long-term problem unless you use that extra time perfectly and build it into something lasting.

Advertisement

The long-term solution is, rather than using your extra money to buy time, you use it to buy freedom.

Let’s say that you were in a situation where you had enough money saved and invested so that the income from those investments could replace your salary. What would you do with your time in that situation?

Advertisement

That’s not “time saving.” That’s freedom, and money can buy it.

We’re kept away from that kind of freedom by the need to earn money, and whenever we use money in a way that doesn’t either create lasting joy or pave our way to this kind of freedom, it’s probably not the best use of that money.

Advertisement

At that point, you have about as much freedom of choice with how to use your time and energy as you can possibly have. You choose what to invest your time and effort into, and if you choose to invest it into things that provide lasting personal joy, you’re going to be building a joyous and personally rewarding life.

Advertisement

Is There a Core?

Once you get beyond that layer, you start to quickly get into issues that involve what you personally value. Perhaps you value your children. Maybe you value a particular hobby, or maybe you really care about a certain social cause.

Advertisement

At that point, you start tying your financial choices directly to those things that you care most deeply about and you begin to see the connections between your choices in each area.

Gradually, that begins to spread to all of your actions. You have only so much time and so much energy. How can you use them most effectively to not only keep yourself alive, but actually have an impact on the things you truly care the most about?

Advertisement

At the outer layers, money appears to be at the center of all things, but after a while you begin to see it for what it is. It’s a medium—a way of exchanging our time and our energy for things we care about. Almost every personal finance problem that we run into comes from making poor trades.

The true core of personal finance, from what I can tell, has little to do with money at all. Spend your time and energy on things you care about.Sometimes, that means accumulating resources so that you can feed, clothe, and house yourself and the people you love the most. Sometimes, it means using your time and energy on the things that really matter to you, whatever they might be.

Advertisement

The best life you can have is all about spending your time and energy on the things that make your life as good as possible, both now and in the future. As far as I can tell, if there’s a core, it’s that, and getting there involves figuring out how to make your trading of time and energy for those other things as efficient and smart as you possibly can.

Trent Hamm is a personal finance writer atTheSimpleDollar.com. After pulling himself out of his own financial crisis, he founded the site in late 2006 to help others through financially difficult situations; today the site has become a finance, insurance, and retirement resource. Contact Trent at trent AT the simple dollar DOT com; please send site inquiries to inquiries AT the simple dollar DOT com. Image byNattanitphoto(Shutterstock).

At the time, she was confined to the pullout couch of her Whidbey Island, Wash., living room, with its view of the Cascade Mountains and Puget Sound. So she had plenty of time to explore the online community where, to her surprise, she discovered she was something of a celebrity.

“It was stunning,” Robin says. “I’m an elder in a community I didn’t know existed.”

Courtesy of Amazon

Robin’s fans belong to an impassioned, mostly millennial movement known online as the FIRE community, or simply FIRE. It’s an acronym that stands for “financial independence, retire early.” Adherents track down to the penny where their money goes, mindful of how much each purchase will really cost, with the idea that dollar amounts should be equated to “hours of life energy,” in Robin’s words. So if you make $300 a day and want to buy a $100 pair of shoes, you ask yourself: Are those shoes really worth nearly a third of a day of your precious time on earth?

As the first part of the acronym suggests, the goal of the movement is to gain financial independence, meaning you’re no longer relying on paid employment to keep afloat.

It’s no coincidence that the ranks of FIRE followers are spreading like, well, wildfire right now: The stock market has been very good to investors in recent years, especially to those who understand the magic of compound interest. Unemployment is low, and opportunities to earn extra money in the sharing economy are plentiful. Add the do-it-yourself spirit of a generation that can learn anything on YouTube, and you’ve got ripe conditions for a movement.

Redefining Career—and Retirement

What’s more, we all know that a traditional retirement is a thing of the past. No one works for 40 years at the same company anymore and retires to a front porch with a gold watch and a pension to show for it. So instead of tweaking the traditional model around the edges, these young people are saying, let’s just blow up the whole concept of career, and retirement, and start from scratch.

The financial independence subreddit has more than 350,000 subscribers around the world. A directory on the blog Rockstar Finance counts roughly 1,600 personal finance blogs, many dedicated to early retirement.

Grant Sabatier, 32, was living with his parents in 2010 and eking out a meager postcollege existence when he came across Your Money or Your Life. “It completely changed my life and trajectory,” he says. “It is still my favorite book of all time.” Sabatier, who says he amassed a fortune of more than $1 million in five years primarily through lucrative web-design side gigs, founded Millennial Money, an online community dedicated to personal finance education and entrepreneurship.

To say Robin is an unlikely financial guru is an understatement. She didn’t spend any time on Wall Street, and she seems more inclined to pass along her favorite kombucha recipe than the name of a favorite mutual fund. She speaks not in the empathetic bursts of Suze Orman but in the melodic voice she uses to sing soprano in a local choir. Her look these days is Golden Girls chic—and while she would seem like a blast to live with, she lives alone above two tenants, whose rent more than covers her housing expenses.

Having paved the original FIRE path decades ago, Robin hasn’t worked for a traditional paycheck in 50 years. After stints as an actress and in film production in New York City, she parlayed an inheritance at age 23 into a modest income that sustained a groovy 1970s lifestyle in which she lived in an “intentional community,” which is kind of like a commune, but less marginalized and more centered around mutual values—”the sharing economy before it was the sharing economy,” she says.

There, Robin taught herself practical skills, from auto repair and hunting to “making booze from dandelions,” a DIY strategy to become self-reliant by acquiring know-how that would enable her to tread lightly and travel cheaply through life.

It was only when people began asking how she lived on so little money that Robin realized she had a story to tell. She and her friend Joe Dominguez, with whom she had lived in the intentional community, teamed up to give financial education workshops around the country. They spread their money values, including planet-friendly frugality, the old-fashioned way in those pre-Internet days. Dominguez, who retired from a brief career on Wall Street at age 31, gave the lectures, and Robin produced them.

The two used their experiences to cowrite the first version of Your Money or Your Life in the early 1990s, a process she says took just nine months. The book first hit shelves in 1992, when she was 47.

The revised second edition of Your Money or Your Life is due out this spring. Robin wanted to write something for today’s millennials, whose prospects she worried were crimped by student debt. She had already begun working on the new draft — without Dominguez, who passed away in 1997 — when she discovered that the original still lived on Reddit; had she known that, she says, she might not even have embarked on the reboot. “It was providential,” she says.

Your Money or Your Life takes readers through a nine-step program intended to transform your relationship with money. It’s not about becoming rich; it’s about figuring out how much is enough. Once you buy less stuff, you won’t need nearly as much money to sustain your lifestyle as you previously did. Wisely invest the difference and wait until the interest thrown off by your portfolio exceeds your expenses. That’s the “crossover point,” Robin writes, and once you reach it, you can peace out of the paid workforce decades ahead of schedule.

The FIRE movement looks at this text as a bible of sorts, one that legitimizes its followers’ path to financial success and offers freedom from being a corporate drone, and ultimately a more satisfying life— a life typically sought after by the 65-and-older crowd. It sounds great. Who wouldn’t want to be in retirement bliss by 40, learning how to make his or her own version of dandelion wine?

But is it realistic?

Vicki Robins wrote “Your Money or Your Life” decades ago. Now she has a whole new fan base.

Photograph by Ian Allen

It’s a very different world today than it was in 1992, when Robin’s book came out. Back then, government bonds—long a favorite source of retiree income—threw off a respectable yield of around 8%. But interest rates haven’t been that plump for a long time, and the 2018 version of the book acknowledges this new reality. Instead, Robin writes about a favorite investment of the FIRE folks: low-cost index mutual funds or exchange-traded funds (ETFs). She also suggests buying real estate, as she has done—in particular, you should consider small duplexes, triplexes, and quads, where you can occupy one unit yourself and have your mortgage covered by your tenants.

Financial Risks

This approach isn’t far-fetched, but it does come with certain risks, according to financial advisors. In order to retire at any age, a general rule of thumb holds that you need to save up at least 25 times your annual expenses. Say you need $50,000 to live on each year—you’ll need to accumulate around $1.25 million in order to withdraw 4% from it each year in perpetuity, adjusted upward for inflation. Robin’s calculations assume a 4% withdrawal rate, with a caveat: “Remember, this is a general example and not specific financial instructions.”

If the stock market posts strong gains, you can wind up with more money than you started with, even as you withdraw your inflation-adjusted living expenses of 4% each year. But if the stock market tanks, and you’re withdrawing on a declining balance, then you face the risk of running out of money.

The 4% rule is a solid method, but it came from research that assumed a traditional retirement of no longer than 30 years, says John Salter, a professor of financial planning at Texas Tech University and a partner in the planning firm Evensky & Katz/Foldes Financial Wealth Management. All bets are off if your retirement lasts 60 years. You’ll have to watch your withdrawals closely and dial back your spending, potentially significantly, if the market declines, he says.

Early retirees also have a longer runway to experience inflation. Prices for regular goods and services roughly double every 25 years, so a 30-year-old early retiree will see general prices rise fourfold over his or her lifetime, Salter says. (Medical costs rise at an even sharper rate.) In other words, you had better hope that stocks continue posting inflation-beating gains.

All the Flavors of FIRE

To be sure, there are many subcultures within the FIRE movement that all have their own spending goals and takes on Robin’s prescriptions. Some are more drastic than others. There’s regular FIRE, for all those people who want to exit the rat race early but might like to occasionally enjoy a good restaurant on the way, or hire a plumber to fix their broken toilet instead of breaking out the wrench themselves. There’s also barista FIRE, for those who might need or want to supplement their savings with a part-time job at a place like Starbucks for the health insurance—a key necessity for early retirees.

On the extreme ends, there are the frugal FIRE adherents, who base a lot of their ideology on the writings of Pete Adeney, a.k.a. Mr. Money Mustache, a FIRE hero who in 2011 started blogging about his retirement at age 30 from his short career as a software engineer and the frugality and DIY spirit that contributed to his success. Adeney, now 43, is so prominent, he’s inspired a loose network of camps in his name. Devotees gather in spots like Gainesville, Fla., and Seattle for Camp Mustache, where talk of churning credit cards for points mixes with traditional camp activities like archery and bonfires. Adeney himself attends the annual Seattle retreat. The $425 tickets for this year’s event, to be held over Memorial Day weekend, sold out last November in less than a minute, as if they were for a Taylor Swift concert.

On the other end of the spending spectrum, you have fat FIRE, for people who want to spend a healthy amount in retirement, maybe because they want to keep living in an expensive city. They have higher savings goals, starting around $2 million, according to a young fat-FIRE devotee in New York City.

Despite their different strains, FIRE walkers have more in common than not. “You’re kind of an oddball in our society if you make a lot of money and choose not to spend it,” says Darrow Kirkpatrick, a former software engineer who retired early at the relatively ripe age of 50.

FIRE folks love meeting up in real life so they can geek out on stuff they might not feel comfortable sharing with friends or family. You know you’ve found your tribe when you can call Roth IRA conversion laddering “beautiful” and have a sea of faces nod earnestly in agreement, as happened at a recent FIRE meet-up in New York City.

For Early Retirees, What Next?

Of course, reaching financial independence is only part of the equation. Once you get there, you have to figure out what to do with the rest of your life—how you’ll spend a retirement that could last 50 or 60 years. That’s a whole lot of downtime, and most people planning on retiring early aren’t thinking about the looming void. “The vast majority are focused on numbers and calculations,” says Grant Sabatier.

He’s now a business partner with Robin in the new website yourmoneyoryourlife.com. He believes many FIRE followers neglect the “spiritual transformation” that can happen when you change your relationship with money. The community remains overwhelmingly male and is heavy on those who naturally organize their thoughts in spreadsheets, like tech types and engineers. Some look down from their huge pile of savings on the masses who, the perception goes, mindlessly go through the motions in their day jobs so they can mindlessly spend on weekends.

Vicki Robin near her home on Whidbey Island, Washington.

Photograph by Ian Allen

Missing is any acknowledgment of the privilege embedded in the ability to save 50% or 75% of your income to begin with. The FIRE movement, to a large extent, remains a culture of “very entitled white men who are very proud of themselves when it wasn’t much of a stretch for them anyway,” says Emma Pattee, 27, a writer based in Portland, Ore., who retired last year at 26 after making successful real estate investments. Many FIRE followers, she says, are already high earners who “disdain all the Midwest minions who can’t get out in front of their truck loan.”

Another unforeseen hazard: Some FIRE bros flame out months after pulling the plug on their jobs. When you’re clocking 14- or 18-hour days at a startup, it’s easy to fetishize a life of home brewing and farming in bucolic Vermont or rural Virginia. But actually home brewing and farming can be lonely and backbreaking work, says Pattee, who knows people who have had to publicly walk back their much-celebrated retirements when the reality fell short of their fantasy. “That’s the problem with just trying to win,” she says.

So how do you fill all those decades when you no longer have to work for pay? It’s not an idle question: There’s a body of research linking early retirement to premature death. “We think it’s not about taking Social Security per se, but it’s about the act of retiring,” says Maria Fitzpatrick, an associate professor at Cornell University, who found that men who retire at age 62 have an increased early-mortality risk of about 20%.

Although her research isn’t on the exact FIRE demographic—after all, it focuses on those who retired at 62 as opposed to 32 or 42—some FIRE followers are well aware of it. Adeney says retiring very early makes it easier to live a longer life than people who retire in their early sixties.

In many ways, FIRE followers are forging into uncharted territory. We don’t have any data on whether extreme early retirees have a tendency to get sicker or even die earlier in greater numbers than their traditionally employed peers, whether they burn out from all the leisure time and return to paid work, or whether they instead live decades in fulfilled contentment, nurturing their passions and giving back to their communities.

Tanja Hester, a FIRE follower who leans toward the frugal strain of the movement and retired late last year at age 38 from her career as a consultant for political and social causes, realizes she’s in a privileged position. “I feel like one of the luckiest people to ever live, and if I can’t use some of it to help others, it will feel like a waste,” she says. She and her husband, who live in the North Lake Tahoe area of California, volunteer at the local humane society and plan to start teaching financial basics in their community.

For her part, Robin gives back by investing in local businesses. Aside from using royalties to pay for cancer treatments in the mid-2000s, she says she’s given away a significant portion of the money she’s made over the years from her bestseller. And she still thinks our society places too much stock in paid work.

She knows the FIRE walkers have an uphill battle, both in their personal finance goals and in the cultural norms they’re bucking. Still, she wishes the best for those who would follow in her footsteps. “If they can endure the identity crisis, then they’re the folks who are woke, and they can take action,” she says. “There’s another generation, hallelujah, that’s adopting these values.”

We’ve included affiliate links in this article. Click here to learn what those are.

These last two articles have focused on how common it is for early retirees to continue making money after they say goodbye to the cubicle. I share stories like that because I’ve seen it happen in so many lives, including my own. Plus, if you do it right, work is fun.

But the downside of all this “side hustle” talk is that you can take it too far, and people start to think that early retirement is possible only if you keep making money afterwards. To the point that I’ve now been hearing many thirtysomething millionaires saying things like,

“Sure, the numbers say I’ve easily reached financial independence, but I’m not even going to touch my nest egg until I’m 60.

So these days, I just do a bit of unpleasant consulting work here and there to cover my expenses and to get the employer subsidized health insurance. “

On top of that, it is hard to get mainstream financial advisers to admit that there is such thing as a finite chunk of money that you can live safely on, forever. They say stuff like, “Financial independence is great, but truly retiring from making money? Forget it.”

Related: your spending can be more efficient if you channel it through a good rewards credit card.

This is where Mr. Money Mustache puts a stake in the ground.

Because it IS absolutely possible and in fact very easy, to make a chunk of money last through your lifetime. There is no magic or unusual risk or hope involved, it’s just plain math.

Even with all the complexities of the modern financial world with its booms and busts, OPECs and Brexits and the churning sea of changing politicians and dictators, it still all boils down to a really simple number. And we can illustrate it with this really simple example:

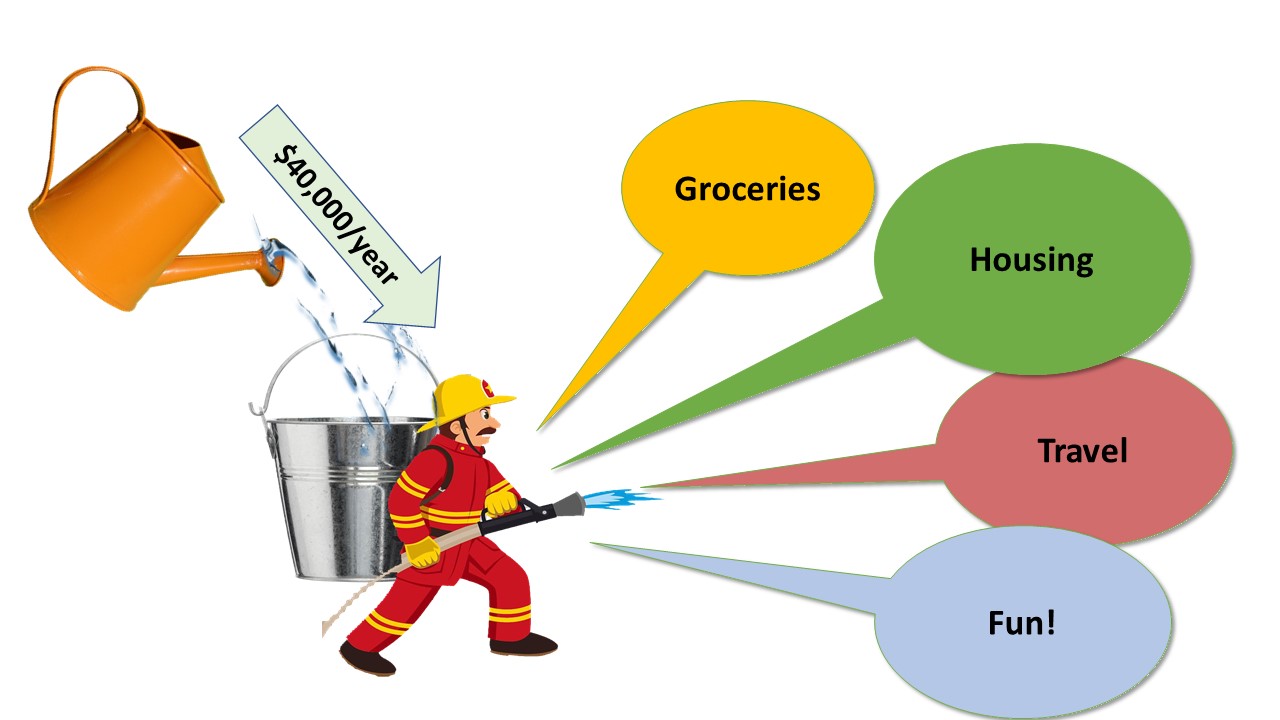

Let’s say you want to be able to spend $40,000 per year, for life, and have that spending allowance continue to grow with inflation. And you never want to make another dollar from work in your lifetime.

In this situation, the following three sentences represent the entire universe of probability for you:

If you retire with $800,000 in investments, you willprobablymake it through your whole life without running out of money (a 5% withdrawal rate)

If you start with a $1 million nest egg (a 4% withdrawal rate), you will very likely never run out of money

If you start with a $1.33 million chunk (a 3% withdrawal rate), it is overwhelmingly certainthat you’ll have a growing surplus for life.

Now, these statements do all depend on the continued existence of a productive human race which continues to innovate and trade and not destroy its own productive capacity.

But you know what?

In the event of a global apocalypse, you won’t be thanking yourself for spending those last few years in the office accumulating a few last shares of index funds anyway.

The strategies described in this blog are designed to shift us all to a more sustainable, healthy, productive economy. So when you live a Mustachian lifestyle, you’re boosting the likelihood of an apocalypse-free future for all of us. Thus, because of you, We are all going to do just fine.

So. A fixed chunk of money is about as safe a retirement strategy as you’ll ever find.

It’s safer than relying on any job, because keeping a steady job depends on the overall economy remaining healthy enough to feed your company, your company remaining solvent, and you remaining productive and useful to that company.

Meanwhile, a good investment portfolio just depends on the world economy in general continuing to exist.

But once you’ve got that chunk, how do actually convert it into a safe stream of lifetime income?

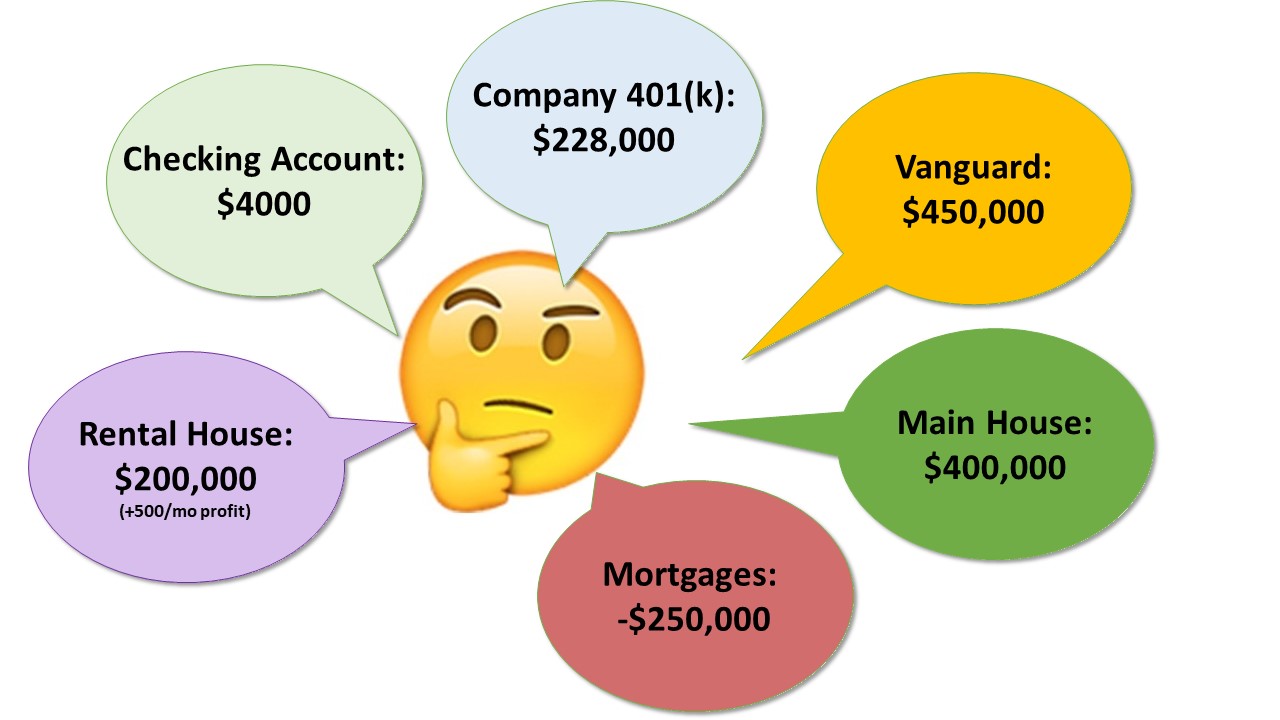

In other words, most of us get to the door of financial independence with something like this:

A complex financial picture with lots of dollar signs – but can you retire on it?

But what we really want is something like this:

This is how money flow really works in early retirement..

So What Is The Problem?

Most people get stuck on the same three questions:

What investments do I use to provide a lifetime of income?

A big chunk of my savings are in 401k or pension, locked up until I’m 59. How do I retire at 35?

How can I pay for (US) health insurance on a $3300 per month budget, when I’ve heard monthly premiums can exceed $1200 per month for a family of four?

The great news is that there are easy answers for all three. They are just not widely known because true early retirement (with no backup income) is such a rare field that very few people write about it. So let’s bang out those answers right here:

Investments:

The Simple Path to Wealth is a short book on investing that convinces you that the simplest strategy is also the best.

As always, I suggest that you only need one thing: a generous bucketload of low-fee index funds. It can even be a single index fund if you want to keep it even simpler: Vanguard’s VTI “Total Stock Market Exchange Traded Fund”

Whether you own these funds through your company’s 401(k) plan, or the brokerage account of your choice, or a Vanguard account, or through an automatic management service like Betterment* as I do, doesn’t matter. What matters is that you are buying pieces of real, profitable companies, which pay dividends and appreciate over time.

Okay, got the funds, Now What?

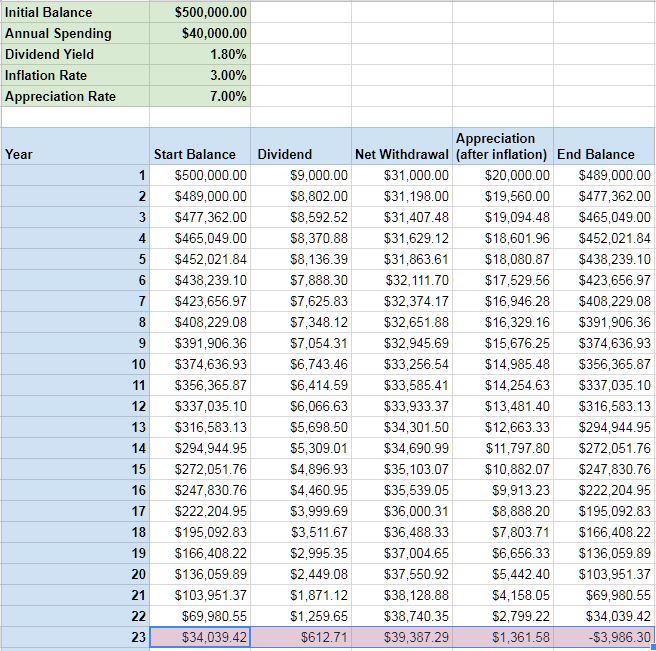

Okay, you’re 35 years old, you have saved exactly one million dollars, and handed in your resignation.

At this point, you will probably have at least two chunks of money: a normal chunk (also known as a taxable account), and a retirement chunk (perhaps a 401k, IRA, or pension).

Let’s suppose it is divvied up like this:

When you retire early, you Use up your taxable accounts first.

On your first day of freedom, you log into your account, find the option for what to do with dividends, and set those to get automatically deposited into your checking account.

Right now, the VTI fund happens to pay a 1.89% annual dividend, which means that the $500,000 account in that green box above will pay $9000 in annual dividends straight to you.

Then, if you’re shooting for $40,000 of annual spending, simply set up an automatic monthly withdrawal of an additional $31,000 per year ($2583 per month) to be sent to your checking account, which is set to automatically pay off your credit card, which you use to buy your groceries.

But Won’t I Run Out of Money If I Do This!?

That’s the magic of early retirement math – the answer is NOPE! Because check out how this plays out:

Because of those withdrawals, your account will lose a few shares every year.

But because of natural stock market growth, your account will be fighting back and each share will be worth a bit more.

Thus, your money lasts much longer than it would if you were just keeping it all in a checking account or stuffed in your mattress.

So a quick spreadsheet simulation of this drawdown reveals that your account survives almost 23 years. At which point you are 58 years old – almost eligible for penalty-free withdrawal of your true retirement money.

BUT, during this whole time, that other $500,000 in your retirement account grew untouched (and untaxed), and it’s now worth about $1.2 million dollars even after accounting for future inflation**. In other words, you have WAY more than enough to live on forever at that point.

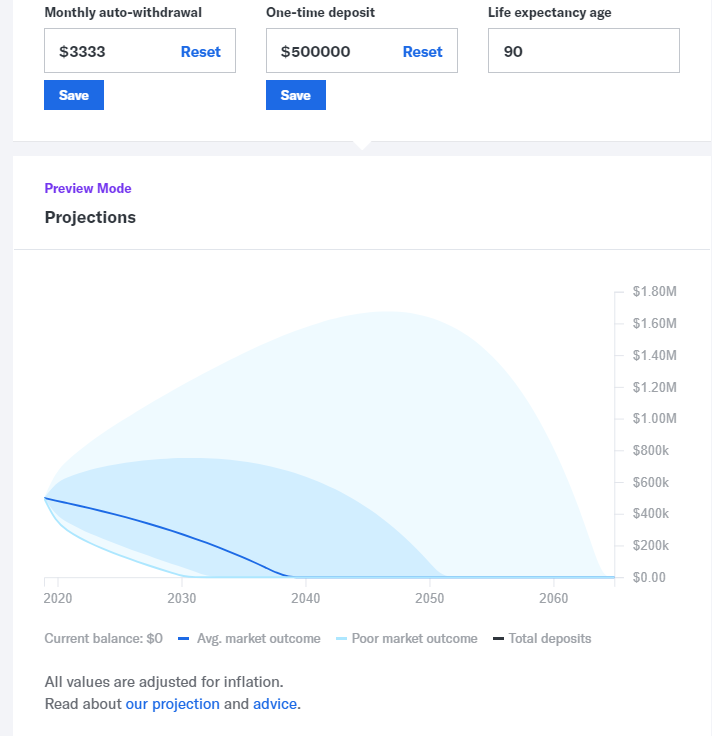

Here’s a quick spreadsheet with simple assumptions and 4% after-inflation stock market returns. In this situation the first 500 grand lasts about 23 years.

And here’s the same thing, except I did it in Betterment’s fun retirement income simulator, using a 95% stock portfolio. This version is slightly less optimistic, but still gets us out to almost 20 years in the most probable scenario.

If you have a really large locked-up retirement balance and a small taxable account, you might want to tap into the retirement account sooner. There are ways to do that penalty-free too, see this earlier MMM article for a few ideas.

The overall lesson: It doesn’t matter how you have your investments split up between normal investments and retirement accounts. It just matters how much you have in total.

Heck, even if you are stuck with a $1 million house occupying a huge part of your net worth, you can convert that into livable money: sell the house, put the cash into index funds, and use the resulting cash stream to rent a spiffy but reasonably priced house or apartment in the lovely walkable area of your choice.

Okay, What About Health Insurance?

If you are stuck in the world’s most expensive medical care market like I am, the most profitable investment of all may be salads, bikes, and barbells because these virtually eliminate the “lifestyle diseases” that trigger about 75% of US healthcare spending.

But even so, most people choose to insure against surprise medical bills, and people with existing medical needs depend on help with those costs.

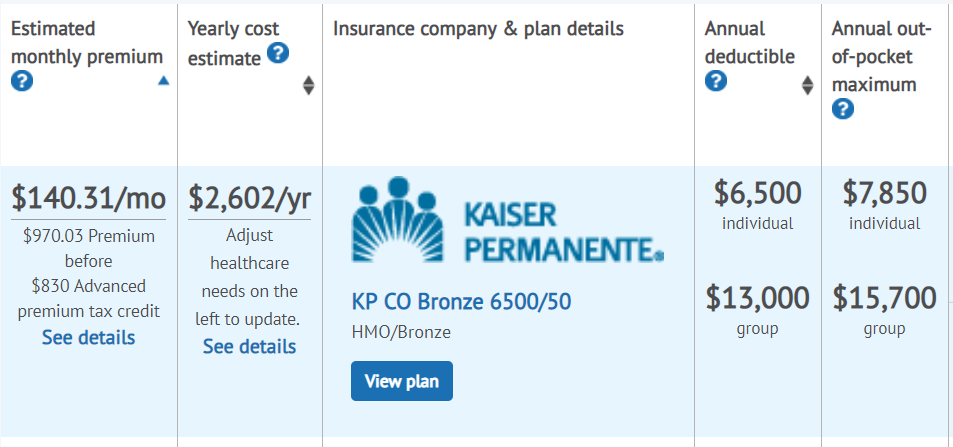

The good news is, the politically controversial Affordable Care Act actually handles this much better than most people assume. If I go to healthcare.gov right now (or in my case the Colorado-specific equivalent) and put in a hypothetical 4-person family with a $40,000 annual income in my zip code right now, I see this:

This represents a cost reduction of $830 per month relative to what a high-income person would pay for the same coverage. So in other words, the United States just has a progressive tax bracket system like other rich countries, chopped up a little differently. It’s not great and to be clear, this is shitty health insurance because it has a high deductible. But at least it’s not a retirement-buster.

Other Things You Probably Don’t Need To Worry About But Everybody Does

What if Stocks fall or My Cost of Living Goes Up?

Stock market crashes are never permanent. In the long run, the market always goes up. So all that happens during a crash is that those few shares that you do sell during those brief times when the market is down, will hurt your account balance just a bit more. Within a year or two, the market is back up and your remaining stocks are more valuable than ever. If you want even further reassurance, you could just choose to spend a bit less money during this time.

As for your cost of living going up faster than inflation – it rarely happens. And if it does, you can adjust by spending less in other areas. Most things are in your control, especially if you take a big-picture view. You can shop around, move, and alter your lifestyle in a million different ways, and in fact this is really good for you.

Standard retirement advice is based on protecting people from any form of hardship or change, which is completely counterproductive. In the right quantity, these are the backbone of a good life and the fuel for personal growth. Without them, you will melt into a whining puddle in front of a television that endlessly blares Fox News.

Every Financial Advisor (even Betterment!) Seems to Suggest Lots Of Bonds, – Why Does MMM Only Hold Stocks?

The quick answer is that stocks earn more money on average, especially right now in 2018 with bond yields so low. Sure, stocks are more volatile, but volatility only bothers fearful people who look at the stock market every day and fret when it jumps around. As a Mustachian, you don’t do this. Lower stock prices are simply a temporary sale on stocks.

What About All Sorts of Other Stuff Not Covered in this Article?

The absolute key to success in early retirement, and indeed most areas of life, is to get the big picture approximately right and not sweat the small stuff. And design the big picture with a generous Safety Margin, which allow lots of slop and mistakes in your original forecasts and allows you to still come out with a surplus.

For example, in the story above I assumed a $40,000 annual spending rate, which is way more than almost anyone really needs to live well here in the US, especially once your kids are grown. I completely ignored Social Security, which will benefit most people at a level between $1000 and $2500 per month for a big portion of their older years. I ignored any incidental income or inheritances or profits you might make on selling your house someday, and the list goes on.

So that’s the line in the sand.

Although I personally think working hard almost every day after your retirement is good for you, it is also completely optional, and you do not have to earn any money at it if you don’t want to.

A chunk of money is a perfectly good retirement plan, and the math doesn’t care if you are retiring at 5 years old or 85. If you get the numbers right, you’re set for life.

—–

*Betterment, Wealthfront, and Personal Capital are investment management systems known as “Robo-Advisors”, which typically buy shares on your behalf and then add on features like rebalancing, tax loss harvesting and personalized advice. I happen to use Betterment because I like the interface and benefit from their tax loss harvesting more than pays for their service fees in my own tax situation.

Betterment purchases a flat rate advertising banner elsewhere on this site, although I don’t get paid for mentioning them or for any new customers they might get. And blog affiliates/advertisers have no say in what I choose to write.

** For this calculation, I assumed the stock market delivers a 4% rate of return including dividends, after inflation. (or roughly a 6-7% total annual return)

When you retire early, you Use up your taxable accounts first.

When you retire early, you Use up your taxable accounts first.